How to deal with a loan in QBO

I have been struggling with setting up and managing a client’s bank loan in QBO and have arrived at a solution which I want to share.

Firstly, QBO – unlike the desktop version – does not have a loan manager feature so a QBO user will have to do the set up and manage the payments manually. Having spent some time speaking to the QBO team at intuit UK, I am aware that this hole in QBO is a bugbear to quite a few. The best suggestion made by them didn’t satisfy me so I have arrived at the following solution.

Step 1 : create an appropriate liability account in the Chart of Accounts

When viewing the COA, click on ‘New’ and choose an appropriate liability account. There are 2 possibilities by default: Loan Payable under Current Liabilities and Note Payable under Non-current Liabilities. The distinction will be seen on the Balance Sheet: the current liability will be paid off within 1 year whereas the long term liability will be paid off over more than 1 year. For most business bank loans a Note Payable liability will be most suitable – though I would rename it Bank Loan or something more meaningful!

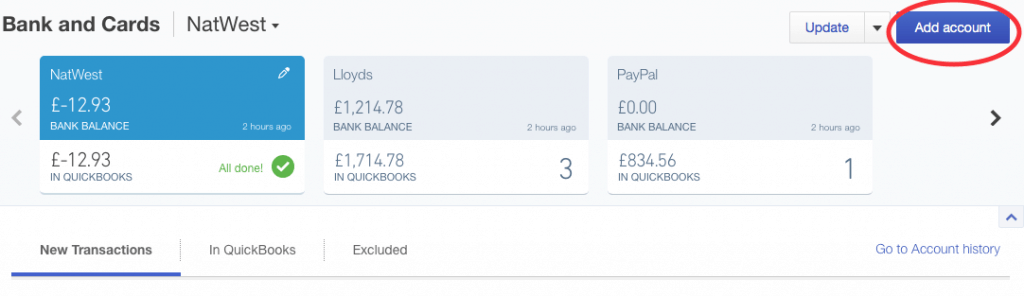

Step 2 : connect the liability account to the Bank’s online banking

There will be a loan a/c with sort code and account number if the loan has been taken out at the bank. Assuming this is the case it is possible to link to this account so that the QBO account will be updated with payments in the same way as any other bank account.

From the Banking screen click on ‘Add account’ and go through the linking authorisation process. At the final stage it is possible to link to the liability account you have created earlier by means of a pull-down list of existing accounts – make sure you do not accept the default which will create another Cash in hand account in QBO.

The loan account will now show on the Banking screen along with the client’s other bank accounts and credit cards.

Step 3 : managing loan payments

A loan payment will come from a bank account which is already in QBO presumably. Therefore it makes sense to see a payment as a transfer from one account to the other rather than as an expense. Starting with the payment from the current account, when adding the transaction to QBO make sure you have selected ‘Transfer’ rather than simply ‘Add’. Make the transfer to the liability account and when it arrives into the synced account it will show up as a Match. Accept this match and the transaction will be imported and the loan account will be suitably credited.

Step 4 : managing interest payments

This is where I ran into difficulties and discovered that QBO will not allow you to add an expense to a liability account. So, when you see an interest charge showing on the loan account you can’t simply add an expense, posting it to an Interest Paid expense account. Oh no – that would be way too simple.

Having spent some time discussing this with the QBO people – and them agreeing that this simple solution would be desirable but confirming that it can’t happen due to a limitation in QBO – I have accepted that I will have to make a journal entry every month to reflect the interest charge. However once the journal entry has been made it will show up on the banking screen as a Match on the loan account which is very satisfying – and confirms that you have the entry the correct way round!

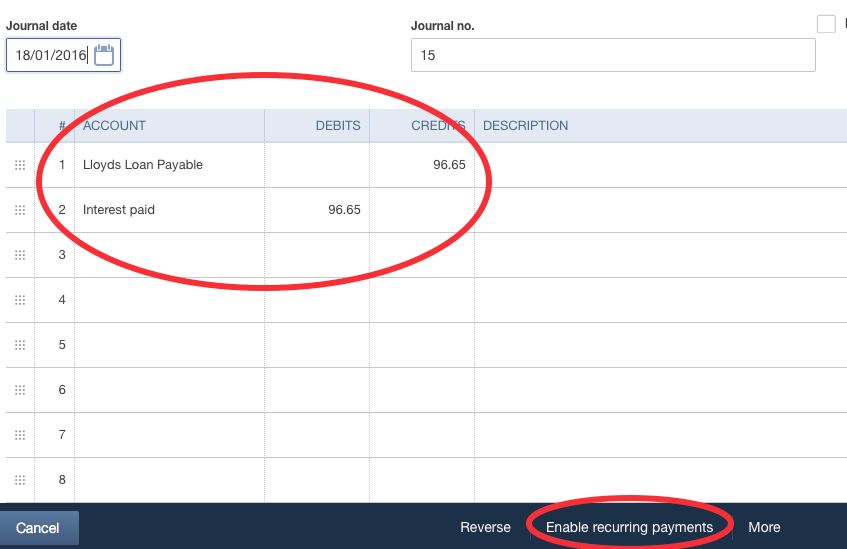

A sample journal entry looks like this:

Don’t forget it is possible to set up a recurring journal entry which will be posted automatically on a given date or day of the week so it should be possible to make this process not too onerous. However you will need to adjust the exact interest payment amount because this will not stay the same month on month.